Section 194H of the Income Tax Act, 1961 governs tax deduction at source on commission and brokerage payments made to residents. The current TDS rate is 2%, applicable when the aggregate payment to a recipient crosses ₹20,000 in a financial year. Both these figures reflect recent changes — the rate was reduced from 5% to 2% effective October 1, 2024, and the threshold was raised from ₹15,000 to ₹20,000 effective April 1, 2025.

For anyone making commission or brokerage payments — whether to sales agents, property brokers, distributors, or other intermediaries — understanding exactly when 194H applies, when it does not, and when the 20% rate kicks in is essential for clean compliance.

What Section 194H Covers: The Scope of Commission and Brokerage

The section applies to any payment received, directly or indirectly, by a person acting on behalf of another. Practically, this covers three broad categories as illustrated in the diagram above:

- Non-professional service fees — commission paid for services that do not qualify as professional services under the Income Tax Act

- Transactions involving goods — brokerage earned in the course of buying or selling goods

- Dealings involving assets — payments related to any asset, valuable article, or thing, with the specific exclusion of securities

Commission is a common feature across real estate, financial distribution, and sales networks. Brokerage typically arises when an intermediary facilitates a deal between a buyer and seller. Both fall under 194H when the other conditions are met — the key distinction is that payments for professional services (covered elsewhere in the Act) and insurance commission (governed by Section 194D) are specifically excluded.

Who Must Deduct TDS Under 194H

Not every payer is required to deduct. The obligation applies to any resident person or entity — including individuals and Hindu Undivided Families (HUFs) — whose total sales, gross receipts, or turnover in the immediately preceding financial year exceeded:

- ₹1 crore in the case of a business, or

- ₹50 lakh in the case of a profession

This means a small trader or professional who has not crossed these limits is not required to deduct TDS on commission payments, even if the individual payment exceeds ₹20,000. The turnover threshold acts as a filtering condition before the deduction obligation even arises.

Payments to non-residents fall outside Section 194H entirely. The section applies exclusively to payments made to Indian residents.

TDS Rate Under Section 194H

The rate structure is straightforward:

| Scenario | TDS Rate |

| Payee has furnished valid PAN | 2% |

| Payee has not furnished PAN | 20% |

| Valid lower/nil deduction certificate under Section 197 | Rate specified in the certificate |

No surcharge, education cess, or SHEC is added to the 2% rate. The 20% rate for missing PAN is a compliance enforcement mechanism — it creates a strong incentive for payees to register and quote their PAN. The threshold below which no deduction is required remains ₹20,000 per payee per financial year (aggregate, not per transaction). A single payment of ₹8,000 does not trigger TDS, but three such payments to the same payee in a year will once the aggregate crosses the limit.

When TDS Is Not Applicable

Several categories of commission or brokerage payments fall outside the scope of Section 194H:

Statutory and government exclusions:

- Commission paid by BSNL or MTNL to their public call office franchisees

- Turnover commission payable by the Reserve Bank of India to Agency Banks

- Payments made by television channels or newspaper companies to advertising agencies for booking or procuring advertisements

Structural exclusions:

- Commission paid by an employer to an employee — this is taxed as salary under Section 192, not under 194H

- Brokerage on transactions in securities (shares on recognised exchanges)

- Insurance commission — governed separately under Section 194D

- Payments for professional services

Procedural route:

- If the deductee believes their income should attract nil or lower TDS, they can apply to the Assessing Officer under Section 197 for a lower deduction certificate. The certificate specifies the applicable rate, the financial year, and a threshold limit. Once issued, the deductor must quote the correct certificate number in the TDS statement and verify that the threshold has not already been exhausted in earlier quarters.

A Supreme Court ruling has also clarified that cellular mobile service providers are not required to deduct TDS under Section 194H on the income or profit component embedded in payments received by their franchisees or distributors from third parties or customers.

TDS Deposit and Return Filing Deadlines

The deposit and return filing calendar for FY 2025–26 under Section 194H:

Quarterly TDS Return Filing (Form 26Q):

| Quarter | Filing Deadline |

| Q1 — April to June 2025 | On or before 31 July 2025 |

| Q2 — July to September 2025 | On or before 31 October 2025 |

| Q3 — October to December 2025 | On or before 31 January 2026 |

| Q4 — January to March 2026 | On or before 31 May 2026 |

Monthly TDS Deposit:

- April 2025 to February 2026 — on or before the 7th of the following month

- March 2026 — on or before 30 April 2026

Two practical examples: TDS deducted on 25 April must reach the government by 7 May. TDS deducted on 15 March must be deposited by 30 April. When TDS is deducted on behalf of the government, deposit occurs on the same day.

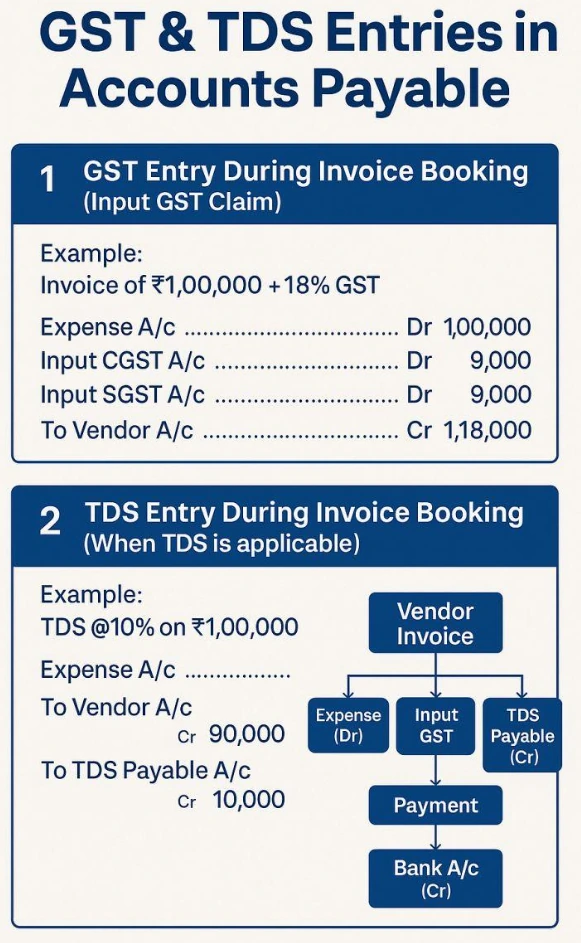

GST and the Commission Amount: A Common Confusion

When the commission or brokerage payment attracts GST, TDS under Section 194H is calculated on the base commission amount only, not on the GST component. The GST is excluded from the TDS calculation. This distinction matters in practice because invoices from agents typically show a combined figure — the deductor needs to isolate the principal commission before applying the 2% rate.

One further point worth noting: even if an agent retains the commission amount by netting it against a larger payment, the TDS obligation on that retained amount still rests with the payer. The retention arrangement does not extinguish the deduction liability — the tax must still be deposited to the government.